{kind=link}

Whilst California strikes to handle regulatory obstacles to truthful, actuarially sound insurance coverage underwriting and pricing, the state’s threat profile continues to evolve in ways in which impede progress, in accordance with the latest Triple-I Points Transient.

Like many states, California has suffered enormously from climate-related pure disaster losses. Like some disaster-prone states, it additionally has skilled a decline in insurers’ urge for food for masking its property/casualty dangers.

However a lot of California’s drawback is pushed by regulators’ software of Proposition 103 – a decades-old measure that constrains insurers’ capability to profitably write enterprise within the state. As utilized, Proposition 103 has:

- Stored insurers from pricing disaster threat prospectively utilizing fashions, requiring them to cost based mostly on historic information alone;

- Barred insurers from incorporating reinsurance prices into pricing; and

- Allowed client advocacy teams to intervene within the rate-approval course of, making it onerous for insurers to reply shortly to altering market situations and driving up administration prices.

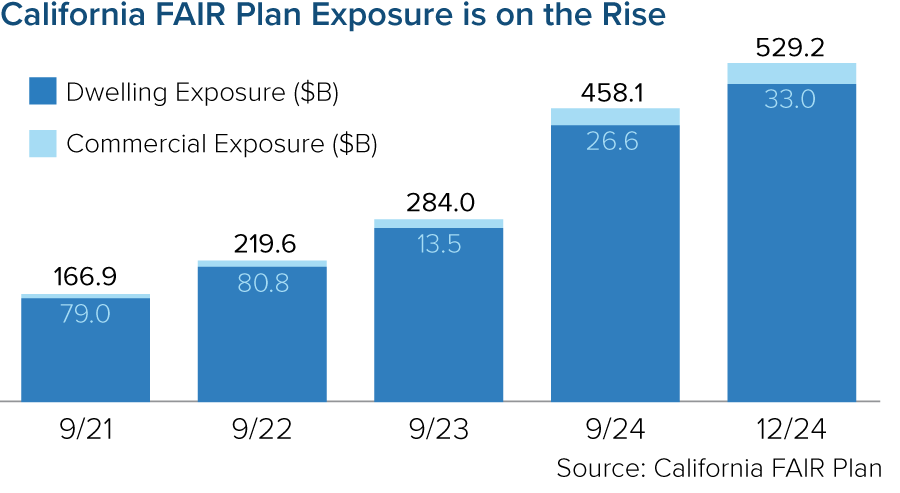

As insurers have adjusted their threat urge for food to mirror these constraints, extra property house owners have been pushed into the California FAIR plan – the state’s property insurer of final resort. As of December 2024, the FAIR plan’s publicity was $529 billion – a 15 % enhance since September 2024 (the prior fiscal yr finish) and a 217 % enhance since fiscal yr finish 2021. In 2025, that publicity will enhance additional as FAIR begins providing larger industrial protection for bigger owners, condominium associations, homebuilders and different companies.

Insurance coverage Commissioner Ricardo Lara has applied a Sustainable Insurance coverage Technique to alleviate these pressures. The technique has generated constructive impacts, however it continues to satisfy resistance from legislators and client teams. And, no matter what regulators or legislators do, California owners’ insurance coverage premiums might want to rise.

The Triple-I temporary factors out that – regardless of the Golden State’s many challenges – its owners really get pleasure from below-average dwelling and auto insurance coverage charges as a proportion of median earnings. Insurance coverage availability in the end will depend on insurers having the ability to cost charges that adequately mirror the complete impression of accelerating local weather threat within the state. In a disaster-prone state like California, these artificially low premium charges aren’t sustainable.

“Greater charges and diminished regulatory restrictions will enable extra carriers to develop their underwriting urge for food, relieving the supply disaster and reliance on the FAIR plan,” stated Triple-I Chief Insurance coverage Officer Dale Porfilio.

With occasions like January’s devastating fires, frequent “atmospheric rivers” that deliver floods and mudslides, and the ever-present risk of earthquakes – alongside the various extra mundane perils California shares with its 49 sister states – premium charges that adequately mirror the complete impression of those dangers are important to continued availability of personal insurance coverage.

Be taught Extra:

California Insurance coverage Market at a Important Juncture

California Finalizes Up to date Modeling Guidelines, Clarifies Applicability Past Wildfire