{kind=link}

In early November, on his radio present, Dave Ramsey provided up some recommendation that was flat out fallacious.

A caller was asking about retiring early and secure withdrawal charges. A brief clip was posted on Twitter/X by Marvin Bontrager wherein Ramsey appeared to get upset and aggravated at certainly one of his personal workforce members, George Kamel, for providing up 3-5% as a secure withdrawal price. (he known as folks silly and morons and have become visibly aggravated and virtually indignant throughout the clip)

The crux of his argument is that 4% secure withdrawal charges are too low. He continued to say that if you will get 12% from the inventory market you may safely take out 8%. Then he began calling folks nerds and dwelling their mother’s basement with calculators and saying 4% is stealing folks’s hope.

Then he, primarily, finishes by saying that one million greenback nest egg ought to create an $80,000 annual revenue perpetually.

Desk of Contents

Beware When Specialists Get Emotional

Do you make your greatest choices if you get emotional? Completely satisfied or unhappy or indignant or no matter – you in all probability would agree that the most effective choices are made if you’re level-headed and never fired up.

You don’t need your monetary advisor to get emotional. You don’t need them to get labored up. You don’t need them to speak about members of their workforce the best way Ramsey did together with his. They are saying that an early and intensely dependable indicator of divorce is contempt. It’s not good for any relationship.

You need somebody who’s calm, collected, and is (if we’re to be completely trustworthy) a calculator-carrying tremendous nerd.

Additionally, watch out each time somebody replaces info with emotion. It’s laborious to have a relaxed dialogue, particularly on air, with somebody who’s getting upset. It’s doubly laborious when that individual is your boss, indicators your paychecks, and has their identify on the wall proper behind you.

8% SWR on $1mm = 67.5% Failure

Dave Ramsey says {that a} $1 million nest egg ought to offer you an $80,000 annual revenue without end.

FICalc is a simple to make use of calculator (you don’t should be an excellent nerd or stay in a basement) that can run simulations and provide you with successful price given your enter parameters. We set the portfolio (its the default) to 80% shares, 15% bonds, and 5% money with a withdrawal price of $80,000 a 12 months.

In 123 retirement simulations, solely 40 have been in a position to maintain withdrawals for 30 years.

If you drop the withdrawal price to $40,000 a 12 months, the success price jumps to 96.7%.

Go forward and play with it your self however the reply is obvious – when you observe Dave Ramsey’s recommendation on withdrawing your nest egg, there’s a 67.5% likelihood you’ll develop into penniless.

Details: A 12% Return is Not Lifelike

The rationale why 8% withdrawal price doesn’t work is as a result of a 12% return shouldn’t be lifelike. It’s basic math.

Dave Ramsey says he makes 12% simply by a decade. You’ll be able to even see Rachel Cruze, his co-host on this clip, attempt to stroll issues again a bit of by discussing what you’d do with a ten% price of return.

Even when you settle for which you can make a median of 12% over a decade, the true killer is what’s often known as sequence of returns threat.

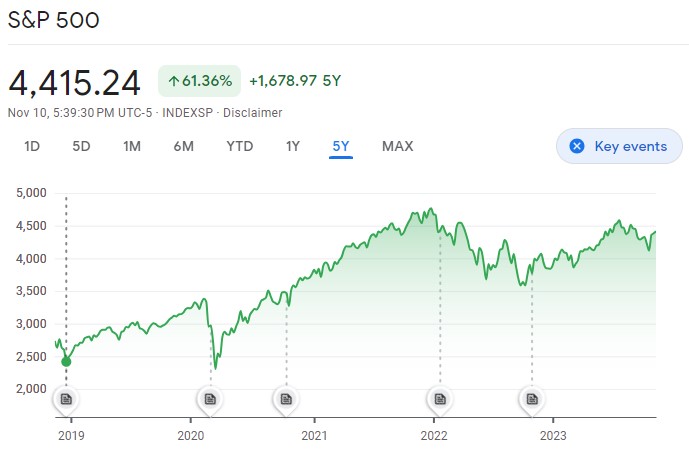

Try the final 5 years of the S&P 500 index:

It’s lumpy. It’s actually lumpy.

In case you didn’t contact your cash (or higher but, stored contributing), you’d really feel nice about making 61% over 5 years. It’s about 10% a 12 months however it’s not 10% yearly.

You’ll be able to see these time intervals wherein the market return nothing. From 2019 to early 2020, when the pandemic hit, we see a return of zero (or much less). From early 2021 to late 2023, you may see how the market went up above 4,500 in late 2021 solely to fall again down beneath 4,000 in 2022.

However if you’re withdrawing frequently, you’re pulling cash out at occasions if you want it for bills. The sequence of returns threat is the danger that you simply’re promoting when the market is decrease. In case you’re retired, you may’t decide and select and so that you’re topic to this threat and it’s what sinks retirement portfolios… particularly these with too excessive of a withdrawal price.

Dave Ramsey is Good At Debt

Dave Ramsey has helped a lot of individuals get out of debt. I used to be by no means in high-interest debt and so I by no means listened to his work or learn his books. I’m conversant in his debt snowball and different debt payoff methods.

What this has highlighted is that when somebody is sweet at one side of one thing (on this case, private finance), it doesn’t imply he’s good in any respect features of the topic.

He has helped lots of people get out of debt. It makes him an amazing skilled to hearken to as regards to debt.

Once we get into investing, that is probably not the case. With paying off debt, you need that emotion as a result of the steps are straightforward and with out nuance. Typically you want a bit of scolding so that you don’t spend if you shouldn’t.

With investing, you need as little emotion as doable and as many calculators as doable.

On this case, Ramsey’s energy seems to be a weak point.