{kind=link}

Since 1980, the Federal Reserve has monitored the value of eggs, milk, beans, orange juice, and different frequent staples of the fridge and pantry. If you wish to examine the year-over-year value of bananas in your space of the nation, you are able to do it utilizing the Federal Reserve Financial Information (FRED) web site. There are dozens of things listed. Scan by the graphs and also you’ll discover some very clear tendencies. Whether or not you have a look at the price of bread, beer, or broccoli, costs are rising.

The speak of a recession appears to be dissipating[i] and the month-to-month inflation price is at the moment in decline, however it’s nonetheless greater than it was in 2020 and 2021, and client and enterprise prices are nonetheless on the rise. That is immediately affecting customers and companies, and their spending decisions. It’s not directly affecting all corporations that compete for private and enterprise prospects.

Nevertheless, value pressures in any space of life may be helpful to corporations that provide the requirements of life, like auto insurance coverage. “How?” you would possibly assume, “Inflation causes the shopping-around syndrome that doesn’t all the time work in our favor.” However prospects, particularly these which can be searching for worth, would moderately make changes and keep inside their present firm than attain out into the unknown. That locations the ball within the court docket of insurers to create new, easy, enticing merchandise and pricing that may help their prospects with value-based choices whereas serving to scale back claims and administration prices. Insurers can redefine themselves and their worth to prospects, they usually can use value pressures to their benefit by performing on the appropriate strategic priorities for his or her companies.

How are private and business auto insurers prioritizing?

The automotive world is quickly altering in all dimensions because of the shift in how different corporations and industries are altering, akin to ridesharing, altering views of car possession, modifications in fleet administration, developments in automotive know-how, and a rising plethora of transportation choices like automobile sharing.

Corporations outdoors insurance coverage are coalescing round a shift to “mobility.” Mobility choices are necessary, however they are often fulfilled by many means past conventional automobile possession. This can be a important shift, impacting enterprise fashions inside each automotive corporations and insurance coverage corporations.

Practically each automotive firm is or is contemplating providing insurance coverage with the acquisition of their autos, both as an insurer or by partnerships with insurers. This development has main implications for business and private auto insurance coverage. Their largest ebook of enterprise could also be in danger if they don’t adapt to a altering market and buyer expectations.

In Majesco’s Strategic Priorities report, Sport-Altering Strategic Priorities Redefining Market Leaders, we have a look at insurer priorities in mild of each market drivers and know-how capabilities. Do insurer priorities meet or exceed buyer wishes? Are they aligned? If not, are insurers contemplating and implementing the applied sciences wanted to fulfill their calls for? Let’s have a look at present insurer priorities.

Customized pricing with knowledge

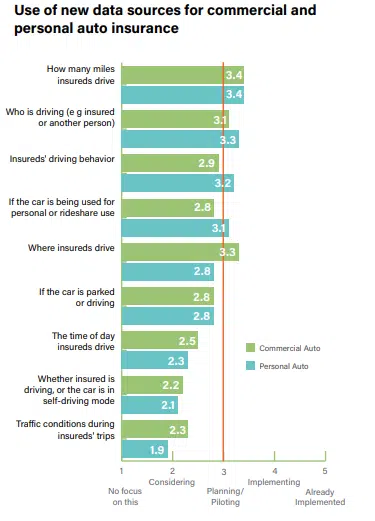

Encouragingly, business, and private auto insurers are way more progressive of their views on new knowledge sources than most different strains of insurance coverage. Six of 9 (67%) knowledge sources or applied sciences are very near the Planning/Piloting section as proven in Determine 1. This aligns with each generational client segments (Gen Z & Millennial SMBs), with over 60% expressing curiosity in most of those choices.

Insurers must speed up their pilots of those six knowledge sources and applied sciences and look extra carefully on the remaining three hovering across the consideration section. Telematics know-how has superior vastly, and it makes new knowledge sources accessible for progressive pricing, in addition to for value-added companies. It’s this knowledge and pricing functionality that would be the market alternative throughout inflationary occasions.

In a Motley Idiot article from Might 2022, they famous that Progressive’s telematics and pricing of insurance coverage insurance policies, utilizing know-how that was rolled out in 2010, is a large benefit over different giant automotive insurers. Since then, they’ve collected important quantities of driving knowledge together with mileage, velocity, braking time, and time of day when driving in order that they now can develop personalised charges for drivers in addition to reductions for protected driving. With over 10 years of driver knowledge, they’ve higher fashions to handle threat, maintain ratios low and meet rising buyer expectations. That is an instance of leaders creating a big market benefit. Different insurers might now be competing towards a 10-year knowledge and expertise benefit.[ii]

Determine 1: Use of recent knowledge sources for business and private auto insurance coverage

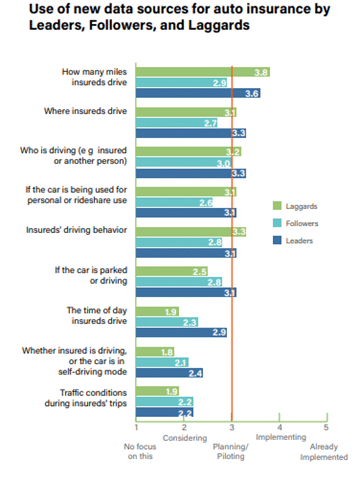

Majesco additionally tracks priorities primarily based on whether or not an insurer is historically a frontrunner, follower or laggard, primarily based on their earlier monitor file for tech adoption.

More and more, insurers are breaking out of their conventional classes. For instance, on this yr’s survey, Laggards are on par with Leaders on 5 of the 9 total auto insurance coverage pricing/underwriting knowledge choices, placing Followers in danger as proven in Determine 2. As a result of the gathering of knowledge over an extended time frame is essential, this places Laggards in a probably aggressive place to problem others available in the market with new, progressive merchandise utilizing these choices.

Whereas Leaders are forward of the opposite segments of their breadth of consideration of the choices, they will take this benefit to a brand new stage by taking a holistic view of driving behaviors and situations throughout the spectrum. This is not going to solely present personalised pricing however will even assist enhance loss ratios and buyer experiences. This might be extra necessary than ever within the coming days. Insurers might want to up their recreation to reach an more and more crowded auto insurance coverage market, the place auto producers have gotten opponents by leveraging the information generated by their autos.

It will imply that insurers might want to use their higher understanding of telematic knowledge AND enhance their knowledge gathering to offer prospects data-fueled worth of their insurance policies. Auto producers might be making an attempt to maintain their insurance coverage acquisition course of so simple as attainable. However auto insurers have levers to drag that producers don’t, akin to huge historic knowledge, auto/dwelling bundling, refined claims processes, and probably wider channels of service that also embrace native brokers. Information is, for each insurers and producers, the lever that have to be employed rapidly and correctly to win and maintain prospects whereas they might be reacting to inflation.

Determine 2: Use of recent knowledge sources for auto insurance coverage by Leaders, Followers, and Laggards

The potential for value-added companies to tip the stability.

Majesco’s survey knowledge reveals that business auto insurers are extra progressive than their private auto counterparts relating to the usage of value-added companies. A number of of those contain offering alerts primarily based on knowledge that insurers have already got or that may be obtained comparatively simply, like reminders about licenses and registrations, alerts about recollects, and updates on automobile market values as proven in Determine 3.

This vary of value-added companies presents “low-hanging fruit” choices to strengthen buyer relationships and meet buyer expectations. And they are often carried out rapidly. As insurers supply telematic applications or insureds have autos with such units, the power to increase value-added companies to prospects turns into simpler, permitting insurers to advertise security and threat avoidance, and assist velocity up claims. For instance, in its This fall 2022 earnings name, Progressive highlighted a brand new app-based Accident Response function that features Crash Detection, extending its pioneering use of telematics past enhancing pricing and underwriting.[iii]

Determine 3: Growth of value-added companies for business and private auto insurance coverage

Laggards should shut the hole on Leaders and Followers with value-added companies.

Leaders and Followers nonetheless have an excellent benefit over Laggards relating to value-added companies. They’ve almost twice as a lot deal with providing a variety of companies. (See Determine 4) This huge hole places them behind and at severe threat of not with the ability to catch up in an already extremely aggressive and crowded auto insurance coverage market. As well as, with the emergence of automotive gamers providing insurance coverage, it will intensify the stress on progress and profitability.

Extra importantly, as our client and SMB analysis reveals, prospects are searching for these value-added companies to assist simplify their lives, but in addition to deal with considerations about value and worth. Now not can insurers rely simply on the bottom value to win enterprise, because it results in a slippery slope of low profitability in addition to a shrinking and sad buyer base. They need to obtain stability, a part of which may be carried out by compelling value-added companies. Worth-added companies are additionally “inflation fighters.” Inflation drives individuals to carry onto their present vehicles a bit longer, particularly if they’ve beforehand had funds and now the automobile is paid off. Updates on renewals, recollects and really useful companies are all value-added companies that private and business auto homeowners will admire. Information on auto worth will even be of excessive significance in order that homeowners can decide when the time could be proper to change vehicles.

None of those companies might be attainable, nonetheless, with out the appropriate framework for gathering, ingesting, and utilizing the information to speak.

Determine 4: Growth of value-added companies for auto insurance coverage by Leaders, Followers, and Laggards

Retaining tempo with channel choices

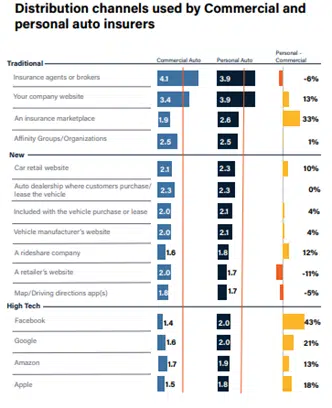

Industrial and private auto insurers are carefully aligned on a lot of the conventional and new distribution channels, reflecting their consciousness of shoppers’ expectations for multichannel buy choices as proven in Determine 5. Private auto insurers usually tend to make the most of insurance coverage marketplaces (33% hole with business insurers) like Examine.com and others, which have grown considerably in use.

Each private and business auto insurers are equally contemplating embedded or partnership channel choices as properly. Whereas private auto insurers are hovering across the consideration section for the Excessive-Tech GAFA corporations, they’re nonetheless forward of economic insurers between 13% and 43%.

Our client and SMB analysis signifies very excessive curiosity in all channel choices amongst Gen Z and Millennials, together with the embedded choices and several other of the GAFA corporations. Whereas insurers are within the consideration section on many of those, they should transfer quickly into Planning/Piloting in the event that they need to sustain with buyer expectations and a rising aggressive panorama with new and present opponents.

Determine 5: Distribution channels utilized by Industrial and private auto insurers.

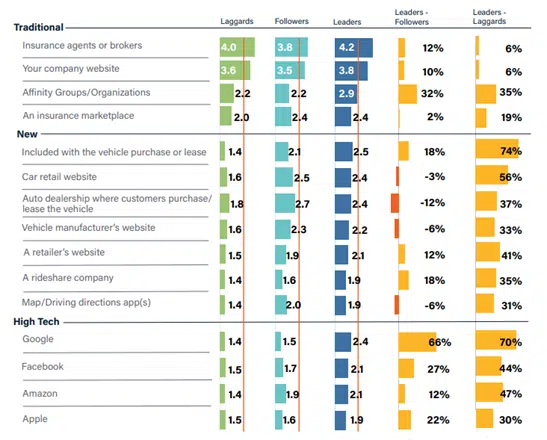

Leaders, Followers and Laggards are carefully aligned of their use of the normal agent/dealer, firm web site, and insurance coverage market channels as proven in Determine 6. Nevertheless, that is the place Leaders separate from the remainder of the pack.

Leaders have sizable leads over each (32%, 35%) in utilizing affinity teams. Leaders additionally dominate over each within the Excessive-Tech channels. Followers maintain tempo with Leaders in all new channels.

Nevertheless, even Leaders shouldn’t see their place as a trigger for consolation. Buyer expectations for these multichannel choices are properly forward of insurers’ present ranges of planning and implementing them, placing them in danger to new opponents coming into insurance coverage.

Determine 6: Industrial and private auto insurance coverage distribution channels utilized by Leaders, Followers, and Laggards

Private and business auto insurers are dealing with a brand new world of competitors, however on the similar time, they’re dealing with new alternatives to refine merchandise, companies, and channels to fulfill their buyer’s need for worth throughout these inflationary occasions.

Majesco helps auto insurers to shift gears, transferring from conventional know-how frameworks, to our P&C Clever Core that embeds and leverages our superior Information Options, Digital Options, and our ecosystem of companions. Whether or not it’s for conventional auto merchandise, shared automobile service, telematics or different choices, now we have labored with insurers who’re innovating and main the way in which. These are the solutions to swiftly assembly the market with aggressive choices that enhance companies and merchandise as they scale back prices. Majesco brings your strategic priorities to life by transferring your organization from consideration to motion. Is it time to compete on the subsequent stage?

For extra info on Strategic Priorities throughout all P&C strains, you should definitely obtain Sport-Altering Strategic Priorities Redefining Market Leaders.

[i] Bartash, Jeffy, The U.S. isn’t in a recession — and it will not be headed for one, MarketWatch, June 6, 2023

[ii] Carlsen, Courtney, “Does Berkshire Hathaway Assume Progressive Is a Higher Auto Insurer Than GEICO?” The Motley Idiot, Might 8, 2022, https://www.idiot.com/investing/2022/05/08/does-berkshire-hathaway-think-progressive-is-a-bet/

[iii] “Progressive (PGR) This fall 2022 Earnings Name Transcript,” Motely Idiot Transcribing, February 28, 2023, https://www.idiot.com/earnings/call-transcripts/2023/02/28/progressive-pgr-q4-2022-earnings-call-transcript/